A buyer’s guide to HUD codes, financing, and long-term value in factory-built housing

Shop any affordable-housing listing site for more than a few minutes and you’ll see “mobile home” and “manufactured home” used as if they’re the same word. They aren’t. One legal date splits these two categories apart, and it changes everything about a property’s safety rating, its financing options, and what it’s actually worth.

That date is June 15, 1976. Everything built before it falls under one set of rules or in many cases, no federal rules at all. Everything built after falls under a strict federal program administered by the U.S. Department of Housing and Urban Development. This guide walks through the construction standards, financing paths, resale value, and zoning realities that separate a mobile home from a manufactured home, and shows where modular homes fit into the factory-built housing picture.

The Great Housing Confusion

Real estate agents, lenders, and even county tax assessors still mix up these terms, which makes the mobile home vs manufactured home question more than just a vocabulary lesson. Getting it wrong can mean applying for the wrong type of loan, under-insuring a property, or misjudging how much a home will be worth in ten years.

The short version: “mobile home” legally refers only to homes built before June 15, 1976. Anything built after that date is, by federal definition, a “manufactured home” regardless of what the seller’s listing calls it.

Below, we’ll compare construction standards, cost, financing, and long-term appreciation for each, then explain how modular homes fit into this picture as a third type of factory-built home.

The Historical Turning Point: What Happened in 1976?

The HUD Code and Factory-Built Homes

Before 1976, factory-built houses on wheels were regulated, if at all, by a patchwork of state and local rules. Manufacturers competed largely on price, and construction quality varied enormously from one builder to the next.

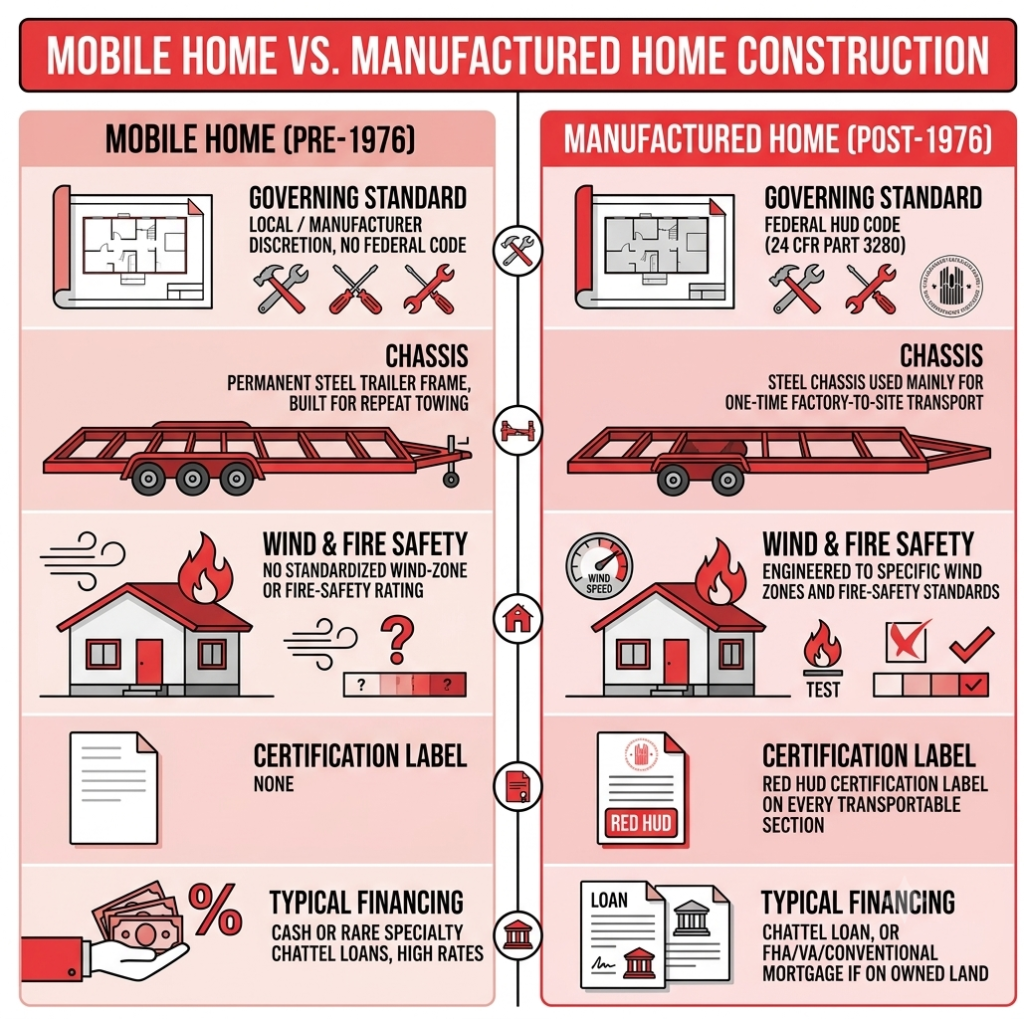

- Pre-1976 (Mobile Homes): Built before federal regulation existed. These units were designed for genuine mobility, sat on a permanent trailer chassis meant for repeated towing, and were not subject to standardized wind, fire, or structural safety rules.

- Post-1976 (Manufactured Homes): Built under the Federal Manufactured Home Construction and Safety Standards Act, universally known as the HUD Code, enforced by the Department of Housing and Urban Development.

The HUD Code sets binding national requirements for structural design, wind resistance by climate zone, fire safety, electrical systems, plumbing, and energy efficiency. It also created an inspection and certification process that follows every home off the factory floor, which is why a true “mobile home” by the legal definition cannot be built today. Every factory-built, transportable home produced in the U.S. since June 15, 1976, is, technically, a manufactured home.

Structural & Design Differences: Under the Hood

Mobile Home vs Manufactured Home Construction

- Mobility vs. Permanence: Mobile homes were built expecting to move from park to park over their lifetime. Manufactured homes are still built in a factory and shipped on a steel chassis, but the vast majority are transported once and then set on a permanent or semi-permanent foundation.

- The HUD Tag: Every manufactured home carries a red HUD certification label riveted to the exterior of each transportable section, confirming it was inspected and meets the federal code. Pre-1976 mobile homes had no such label.

- Size Options: Modern manufactured housing comes in single-wide, double-wide, and triple-wide configurations, each shipped in sections and joined on-site, giving buyers far more floor-plan flexibility than older single-wide-only mobile home stock.

Here’s a side-by-side look at how the two categories compare structurally and legally:

Feature | Mobile Home (Pre-1976) | Manufactured Home (Post-1976) |

Governing Standard | Local/manufacturer discretion, no federal code | Federal HUD Code (24 CFR Part 3280) |

Chassis | Permanent steel trailer frame, built for repeat towing | Steel chassis used mainly for one-time factory-to-site transport |

Wind & Fire Safety | No standardized wind-zone or fire-safety rating | Engineered to specific wind zones and fire-safety standards |

Certification Label | None | Red HUD certification label on every transportable section |

Typical Financing | Cash or rare specialty chattel loans, high rates | Chattel loan, or FHA/VA/conventional mortgage if on owned land |

One practical safety checklist worth running through before buying any factory-built home in a wind-prone region:

- Confirm the home’s wind zone rating matches or exceeds your local requirement.

- Check that tie-down and anchoring systems are installed to the manufacturer’s specifications.

- Verify the HUD data plate inside the home lists the correct wind, snow-load, and thermal zone for your location.

Financing and Legal Status: Personal Property vs. Real Estate

Mobile Home Financing and Loans

This is where the mobile home vs manufactured home distinction hits buyers’ wallets hardest. How a home is titled, not just how it was built determines what kind of loan you can get.

- Chattel Loans vs. Traditional Mortgages: If a home is not permanently affixed to land the owner controls, it’s classified as personal property, much like a car or a boat, and financed with a chattel loan. Chattel loans typically carry higher interest rates and shorter terms than a mortgage.

- Converting to Real Property: A manufactured home can be reclassified as real estate once it’s placed on a permanent foundation on land the homeowner owns and the title is retired with the state. That reclassification opens the door to FHA, VA, and conventional mortgage financing.

- The Pre-1976 Financing Hurdle: Lenders treat true mobile homes as a high-risk asset class. Conventional mortgages are essentially unavailable, and even chattel lenders are selective, since the homes lack any HUD safety certification.

On the manufactured-home side, secondary-market guidelines have caught up with the product. Fannie Mae’s MH Advantage and Freddie Mac’s CHOICEHome programs extend conventional, mortgage-style financing including lower down payments to manufactured homes built to specific design and durability standards and permanently affixed to land owned by the buyer.

Cost, Appreciation, and Long-Term Value

Manufactured Home Value and Investment

- Upfront Costs: Factory construction trims labor and weather-delay costs, putting manufactured homes roughly 35–50% cheaper per square foot than comparable site-built homes, according to U.S. Census Bureau cost data on new construction.

- Do They Appreciate?: The idea that all manufactured homes lose value like a car is outdated. Appreciation comes down to three factors: whether the home sits on owned land, the strength of the local real estate market, and how well the home has been maintained.

A manufactured home titled as real property on owned land, in a market with rising land values, can appreciate similarly to a site-built home. A manufactured home in a leased-lot community, by contrast, behaves more like a depreciating personal-property asset, because the buyer never owns the land underneath it.

Where Do Modular Homes Fit In? (The Third Competitor)

Modular Homes vs Manufactured Homes

Any honest manufactured vs modular home comparison starts with the building code each one follows, since that’s the single biggest legal and structural difference between them.

- Different Code, Different Category: Manufactured homes are built to the federal HUD Code everywhere in the country. Modular homes are built to the same local, state, and regional building codes that apply to traditional site-built houses; there’s no separate federal modular code.

- Assembly: Modular sections are built in a factory, trucked to the home site, and assembled with cranes onto a permanent foundation, then finished by local contractors to meet code.

- Financing and Appreciation: Because modular homes are inspected and classified under the same codes as site-built houses, they’re treated as real property from day one and typically qualify for standard mortgages, with appreciation patterns closer to site-built homes than to HUD-Code manufactured housing.

So when someone asks “modular or mobile home?” or “modular vs mobile home,” the comparison isn’t really close: a modular home is built to local residential code and treated as real estate, while a mobile home predates federal safety regulation entirely and is treated as personal property. The more relevant modern comparison for most shoppers is manufactured vs modular, since both are factory-built but governed by different codes, different financing rules, and different appreciation potential.

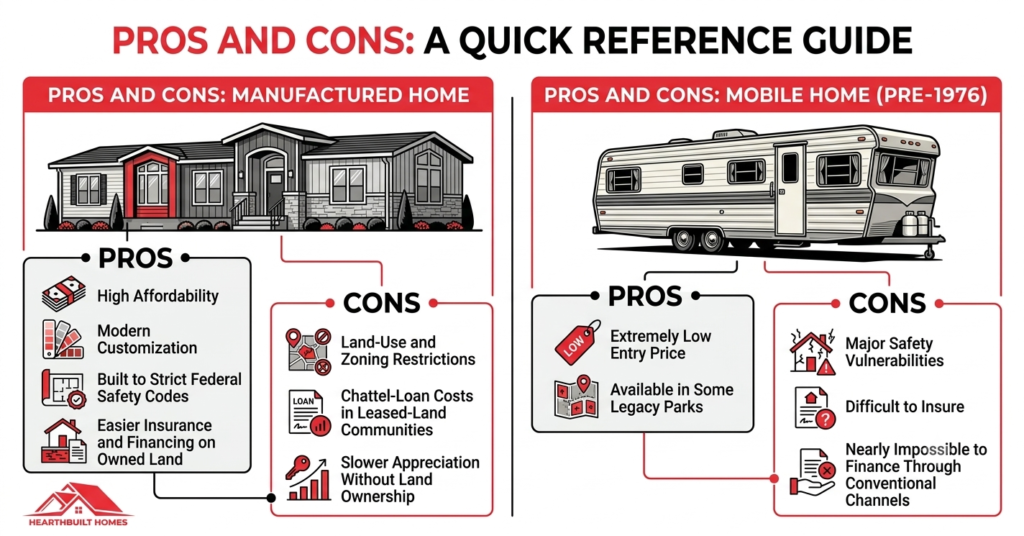

Pros and Cons: A Quick Reference Guide

Choosing the Right Factory-Built Home

Manufactured Home | Mobile Home (Pre-1976) |

Pros: High affordability, modern customization, built to strict federal safety codes, easier insurance and financing on owned land. | Pros: Extremely low entry price, available in some legacy parks. |

Cons: Land-use and zoning restrictions, chattel-loan costs in leased-land communities, slower appreciation without land ownership. | Cons: Major safety vulnerabilities, difficult to insure, nearly impossible to finance through conventional channels. |

Conclusion & Next Steps

People will keep using “mobile home” as a catch-all term, but the legal and financial reality is more precise. A true mobile home is a pre-1976 relic with real safety and financing limitations. A manufactured home is a modern, federally regulated product that can perform like a smart long-term investment when it’s placed on owned land and properly maintained. A modular home, meanwhile, sits closest to a traditional site-built house in both code compliance and financing.

Before you sign anything, pull the property’s zoning designation and confirm whether the land is owned or leased, since that single fact drives nearly every financing and appreciation outcome described above. Then talk to a lender who specifically underwrites manufactured and modular housing, not just a generalist mortgage broker so you know exactly which loan programs, down payment requirements, and insurance rules apply to the specific home you’re considering.